Print

Print ![]() Comments Off on 2020 Activist Investor Report Print

Comments Off on 2020 Activist Investor Report Print ![]() E-Mail Tweet

E-Mail Tweet

Aniel Mahabier is CEO and Folorunsho Atteh is Senior Corporate Governance Analyst at CGLytics. This post is based on their CGLytics memorandum.

There has been a surge in activist interventions at companies around the world, and there has also been a broadening of focus—activism is no longer the sole province of hedge funds and other specialized investors; activism is now not just seeking to unlock value, but also to intervene in governance and performance areas.

As institutional investors embrace activism at companies in their portfolios, activist campaigns begin

to focus on:

This trend marks a major expansion of both the types of investors who intervene as activists, and the target of such interventions.

Activist investors seek to unlock value. For example, hedge fund Elliot Management in 2016 campaigned for Samsung Electronics to return US$10 billion to shareholders. [1] In 2018, Elliot successfully campaigned for Hyundai to cancel its planned corporate restructuring, and to increase the dividend. [2] This is a classic activist campaign to unlock value, meaning to obtain more for shareholders.

An activist entity will buy a material stake within a company, mobilize other influential investors for their campaign, and then seek to enforce their own goals for the company. The mechanisms through which they seek to achieve their goals often include:

Activist shareholder campaigns first started in the U.S. but are now finding fertile ground in the APAC region, the UK, and, to a much more limited extent, continental Europe.

There has been growth in the number of campaigns launched by investors engaging in activist activities from 2017 to today.

In 2017, there were:

This equates to a 34% rate of success. It is worth noting that of the activist campaigns 34% were either unsuccessful or withdrawn by the investors involved, while 32% of the campaigns were announced but were unable to gain traction or were ongoing.

Such was the case of Change to Win Investment Group (CtW), which in 2018 led a “Vote No” campaign against three members of the board at Tesla; officials with five state or municipal pension funds joined with CtW in the campaign after expressing serious concern about the board’s level of independence and other governance issues. [3] The “Vote No” campaign, however, ultimately failed.

In 2018, activist investor activity increased:

2019 saw a sharp increase in activist campaigns launched:

Campaigns carried out in 2020 (so far):

Amicable agreements became more common in 2018, perhaps as a result of boards becoming accustomed to activism and reacting to it more effectively. In 2018, amicable agreements went up to 197 compared with 164 in 2017, representing a 20% increase.

Nonetheless, the number of successful activist investor campaigns remained largely the same in 2018 from the previous year, with 100 successful campaigns compared with 101 in 2017.

However, the number of successful campaigns dropped by 15% in 2019, falling to 85 successful campaigns, while the combined number of successful and settled campaigns was 149, showing a 24% drop in success rate for activist investors.

In contrast, the number of unsuccessful campaigns increased by 34% in 2019 to 185 from 132 unsuccessful campaigns in 2018.

Campaigns carried out so far in 2020 shows an overall increase in the number of campaigns, as we are only part way through the year. However, successful campaigns currently stand at 44 which represents 6% of total campaigns, while settled campaigns stands at 31, representing 3%. Activist investors have not been successful this year.

The number of failed campaigns in 2020 is at 283, representing 53%, which is 65% higher than the number of unsuccessful campaigns in 2019. One example of a successful proxy fight this year was Starboard Value LP’s campaign at GCP Applied Technologies where eight of its Director nominees where successfully elected at the company’s AGM.

Whether activist campaigns are successful or not, it is important to note that any activist campaign brings negative publicity, takes time to arrange, and in many ways disrupts the activity of a business and its management.

Hedge funds and private equity firms are the traditional activist investors, but there are new types of companies involved, with new targets. Over the past decade, institutional investors have become more active in seeking changes to companies’ governance structures, without necessarily seeking to unlock value and redistributions to shareholders.

One recent example out of many, is the case of California State Teachers’ Retirement System (CalSTRS) which became increasingly frustrated with the board of Netflix as its board failed to replace directors after significant opposition from shareholders and disregarded 17 majority-supported shareholder proposals. [4]

At the AGM in 2018, CalSTRS and other shareholders supported a proposal from a group of pension funds representing retired New York City employees, and the Connecticut Retirement Plans Trust Fund to grant proxy access, and allow shareholders to nominate their own slate of directors. Shareholders also supported a proposal from CalSTRS to allow investors to make change through a simple majority vote.

We are seeing traditional investors change their position rapidly from passive to active engagement. The surge in activist activities in 2020 may be ascribed to these new actions, and it is widely expected that this trend will continue.

Instead of seeking a direct release of value to shareholders, activists are campaigning to improve corporate performance—obviously, a different route to the same goal.

Governance issues such as shareholder rights, board tenure, independence, diversity, and expertise are all issues to improve performance, and so are attracting activist attention.

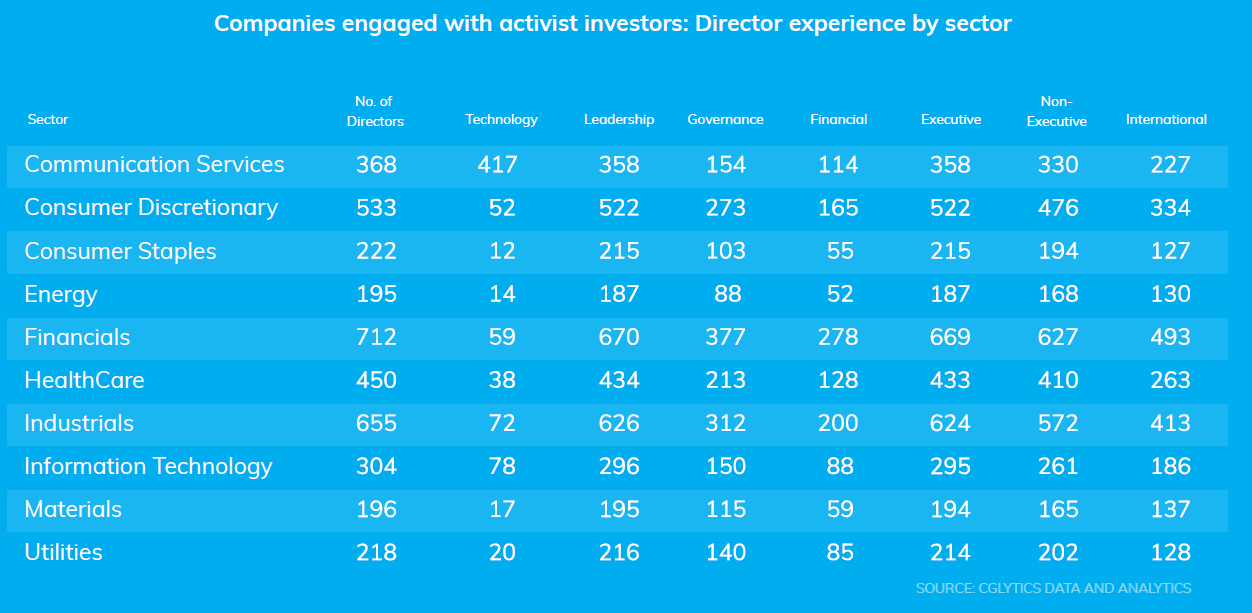

CGLytics pulled the governance data of 368 companies within its global coverage that are currently engaged with Activist Investors, driven either by governance matters, strategy, or M&A. One of the reoccurring issues that is being discussed within the investment community is whether board members have the requisite skill set to effectively carry out their oversight function over the management team. Activist investors have often questioned the experience of board members of the companies they have targeted overtime. This may be related to the fact that the individuals are not the right fit for the company, or the board lacks the expertise needed to formulate strategy for the company.

Investors seek to know if board members have experience as Executive or Non-Executive membership on other boards, experience as leaders, in international finance, governance, technology and in the sector in which the company operates.

Companies should operate with a board matrix that lays out the ideal skill set for the board. This is not the case, as CGLytics data shows that board composition is lacking at many organizations.

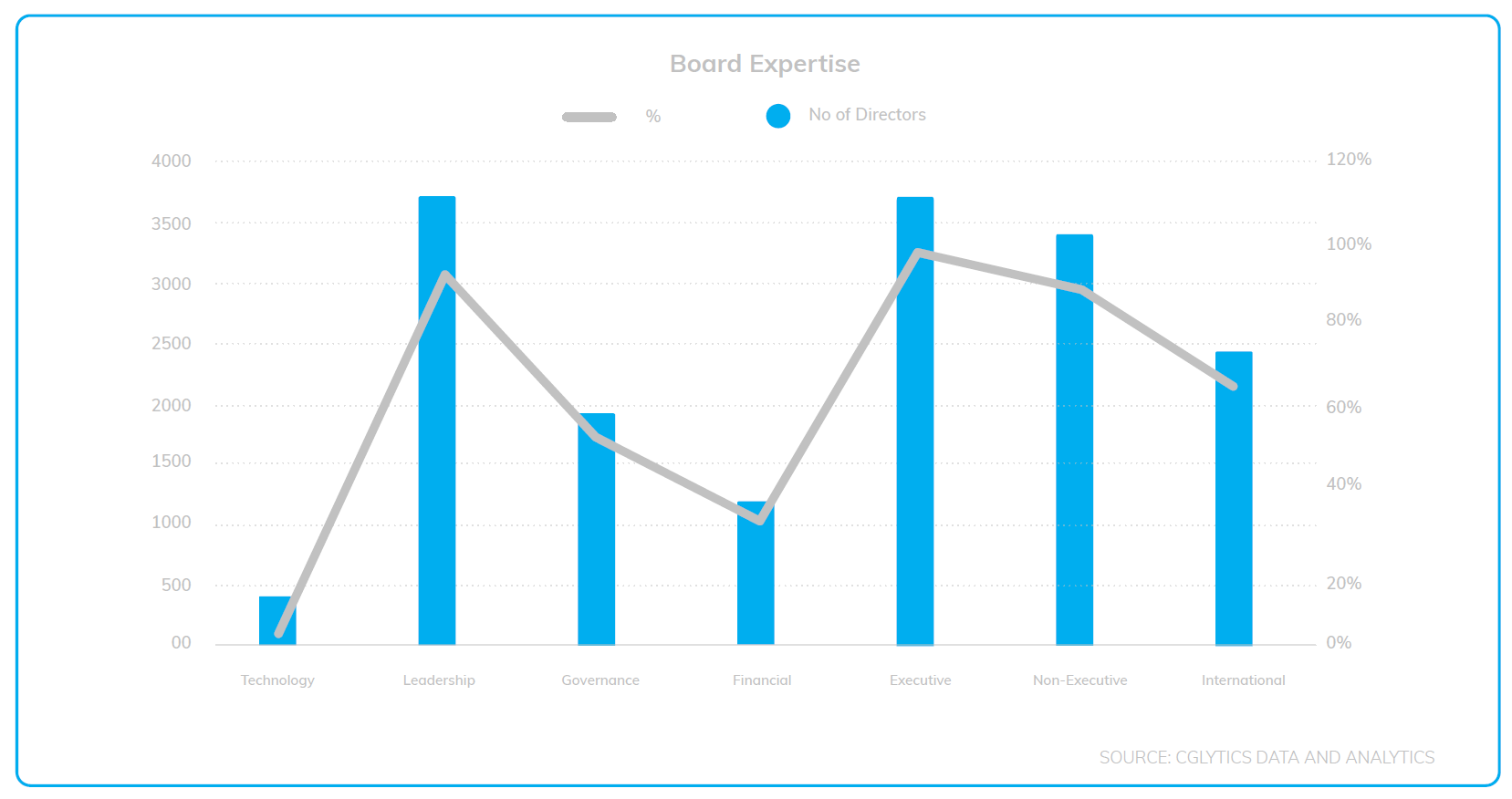

Data from CGLytics Board Insights of the 368 sample companies reveals that all boards in the sample have members with requisite Non-Executive, Executive, Sector Experience, International and Leadership. But many lack members with experience in Finance, Governance and Technology.

Finance, governance and technology are the skills needed in the current business climate. But our data shows that only 11% of the 3,853 directors in our sample have technology experience; 50% (1,925) have governance experience and just 32% (1,224) have financial expertise.

The one area in which a large number of the companies in our sample have experience is finance: All but 9 companies have at least one board member with financial expertise, and 325 of the 368 companies in our sample have between one and five board members with financial expertise. 141 companies have between four and eight members with financial expertise.

A full 148 of the 368 companies in our sample do not have board members with technology experience, 201 of the 368 companies only have between one and three board members with such experience. Two companies, however, Alphabet and Leaf Group have seven and eight board members with requisite technology experience respectively.

Following the 2001 Enron Crisis and the 2008 financial crisis, corporate governance demands that at least one board member should have financial expertise. The definition of what qualifies someone as a financial expert has, however, evolved since then. Under the SEC guidelines, for an individual to be deemed a financial expert, he/she must have worked in a company as a principal financial or accounting officer, controller, certified public accountant, or auditor.

French and UK corporate governance accepts an individual who has been a member of the audit committee as having sufficient financial experience, with competence in finance or accounting. The audit committee members should have the skills required to assess the performance of companies and external auditors as well as the ability to evaluate financial statements.

To be categorized as a corporate governance expert, the board member is expected to have worked as a company secretary in legal and regulatory compliance, or to have served extensively as a member of the governance committee within a company. The board member should be able to recognize non-compliance or governance risks.

In last decade, technology has been an integral part of how companies across all sectors conduct business, and the need to have board members who understand it is mandatory. A board member with this expertise is expected to have extensive experience in information technology, software development, digital, cyber security, and other IT related departments.

A look at the distribution per sector shows that Consumer Staples, Energy, Materials and Utility are lagging in the number of directors with technology expertise. This is the same for governance expertise, where Energy and Consumer Staples have the smallest number of directors with the requisite skills. Energy, Consumer Staples, Materials and Utilities also have the smallest number of

directors with financial skills.

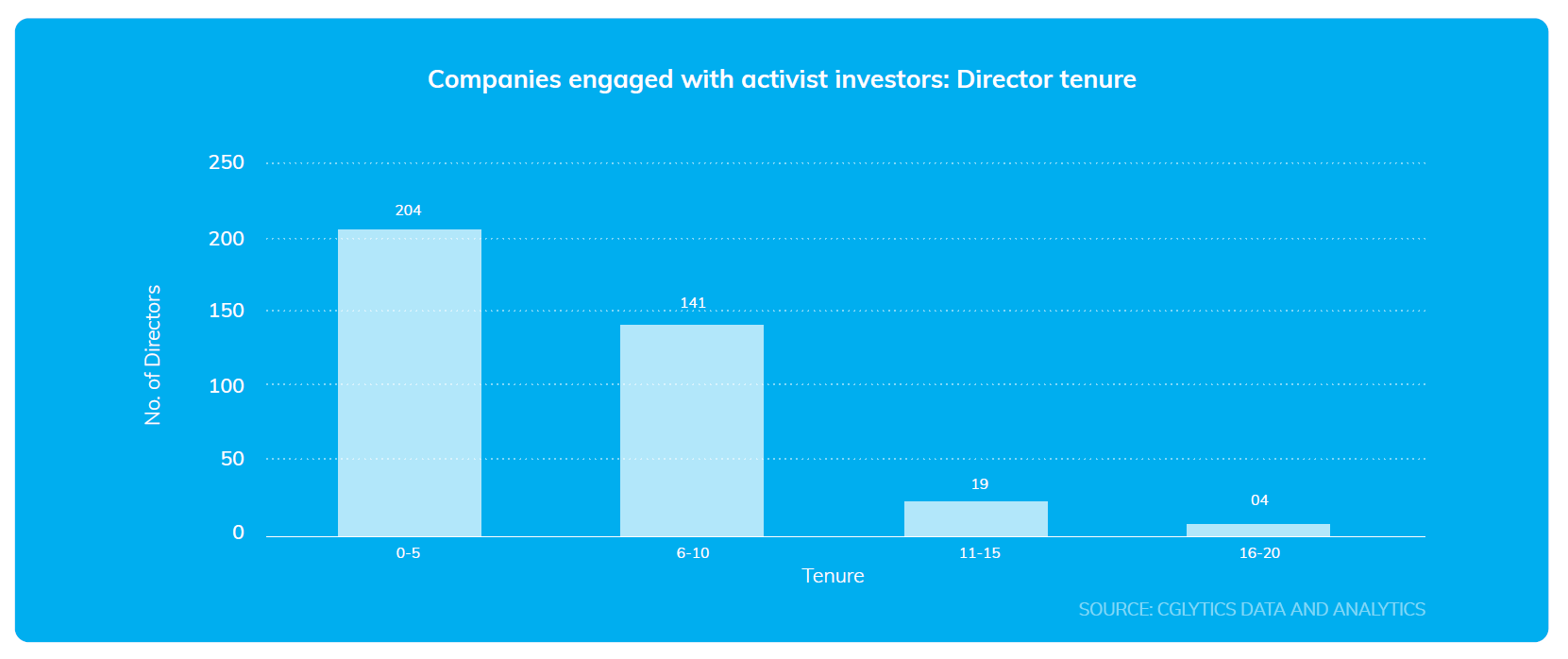

The age of board members is also a factor in corporate performance. When directors have long tenure, they tend to become cohesive with management, and this erodes their ability to oversee performance.

Boards dominated by older members tend to be out of touch with current trends. Younger board members bring new ideas to the table. Investors are therefore pressuring boards to bring in younger members.

From the 368 sample companies, the average tenure is six years. This is a healthy average for the sample companies, with directors tenured between zero to five years making up 55% of the sample.

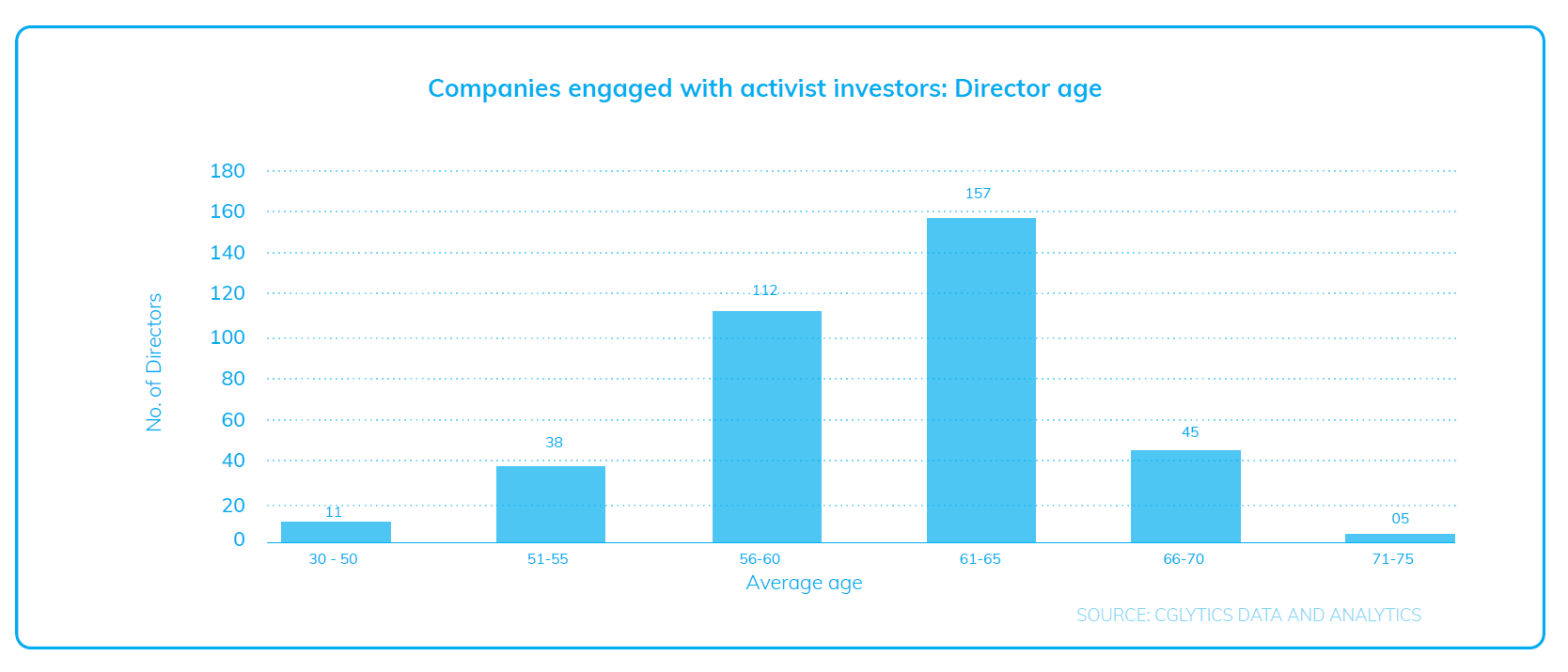

Data available also shows an average age of 61 years among the 368 sample companies with 55% of the board members aged between 61 and 70, 41% aged between 51 and 60 while the youngest being 35 and the oldest being 75 years old.

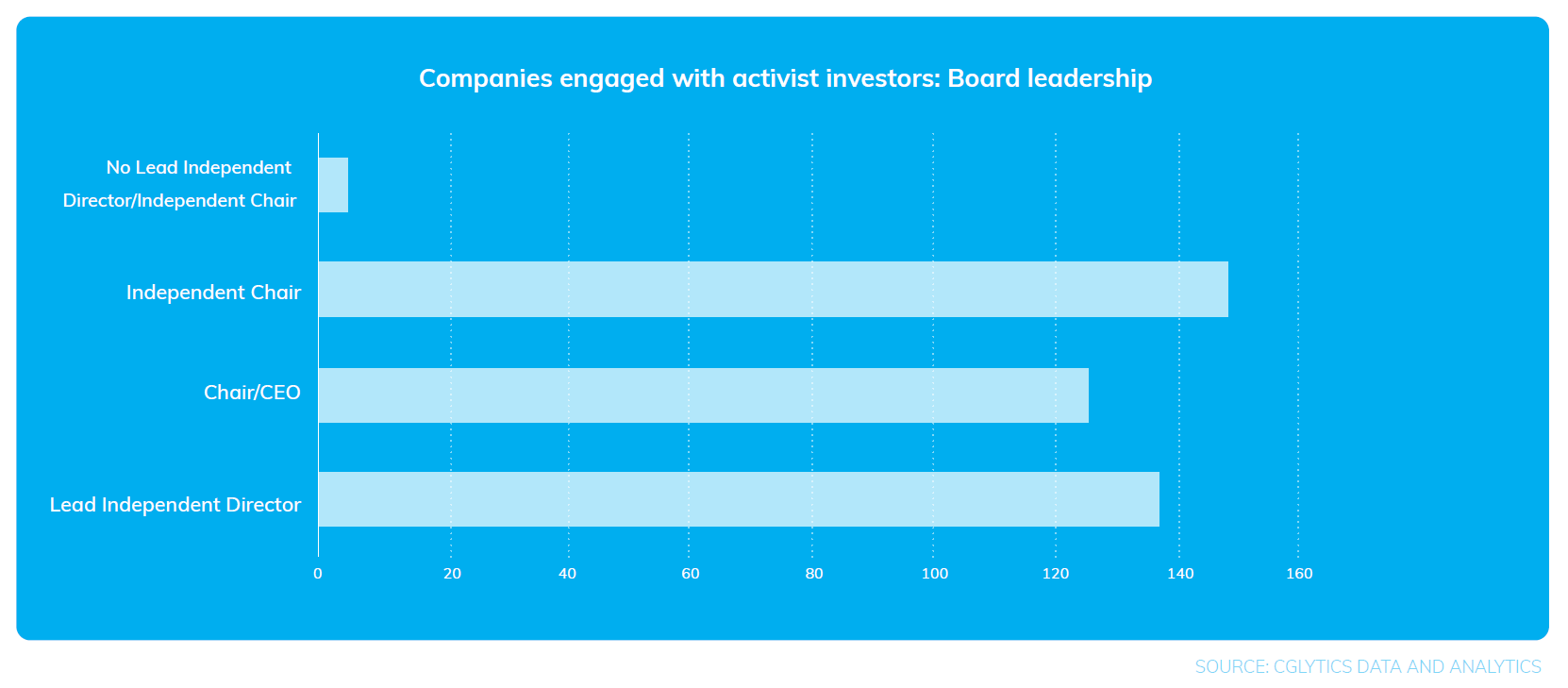

Board independence and leadership structures may also attract activism. Majority of the target companies being considered in this report have independent boards as it is defined in corporate governance. However, there are instances where the leadership structure adopted has attracted shareholder scrutiny.

CGLytics data shows that, of the 368 companies in our sample, 126 have combined Chairman/CEO roles—which is seen as poor corporate governance practice—while 137 have Lead Independent Directors (LID), and 149 have Independent Chairs, while four do not have Lead Independent or Independent Chair roles.

Some companies are controlled, and some choose not to have a LID or Independent Chair. New York State Common Retirement Fund put forward a proposal at the 2019 annual general meeting of ExxonMobil for an Independent Board Chair, which garnered 40% from voting shareholders; a slight increase of 2% from 2018 which was supported by 38% voting shareholders. Another example: In 2018, Pernod Ricard announced the appointment of a LID and new strategic plan after it was targeted by activist investor Elliot Management.

Controlled companies often show disparities in shareholder rights. A prime example is Facebook, whose majority shareholder and co-founder Mark Zuckerberg controls 13% of the economic rights but 57% of voting rights. This makes it almost impossible for activist or dissident shareholders to have any meaningful impact, as shareholder proposals (with respect to equal voting rights and independent chairs) have failed over past four years. Nevertheless, this has not stopped shareholders from pushing for changes in the company.

Shareholders have protested the re-election to the board of Marc L. Andreessen, who is seen as a Mark Zuckerberg ally. In 2016 and 2019, 16% and 11% of voting shareholders voted against his re-election.

Activists may also target M&A and strategy in an effort to improve corporate performance.

In 2020, out of 797 activist campaigns, 59 targeted M&A issues and 155 targeted strategy at companies where growth and profitability were in question.

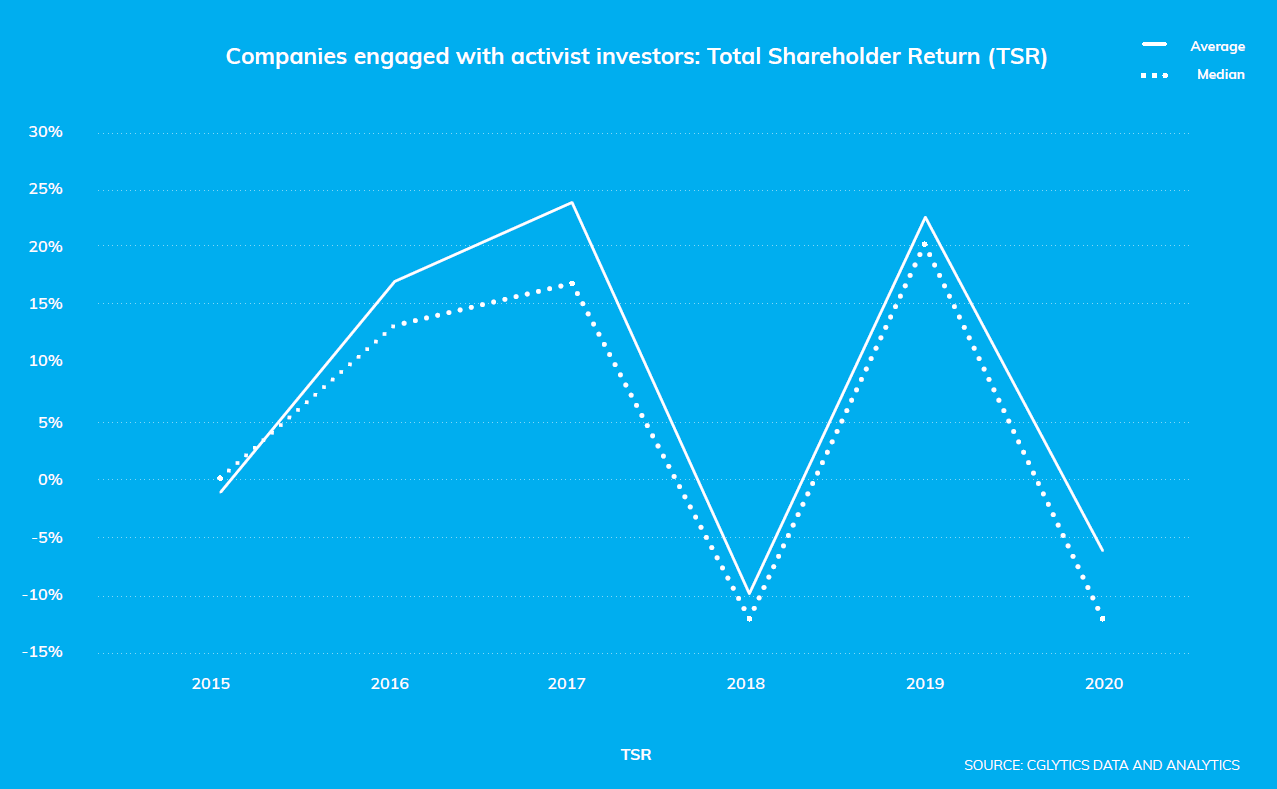

CGLytics has captured three key growth and profitability indicators that attract activist attention. We have identified Total Shareholder Return (TSR) as a key indicator for activism; TSR is used to measure the long-term value of companies and it has been the most accurate metric for gauging success. Changes in the TSR of the companies in our sample are shown in the chart below.

Mersana Therapeutics, Inc. has the best average TSR over a five-year period at 128%. On the other hand, Amigo Holdings PLC is rock bottom with a five-year average of -84.91%.

Overall, 128 companies have negative median TSR with an average of -18% while 119 have negative average TSR with an average of -13%. 247 stayed positive with an average of 17% out of which 145 averaged less than 15%.

The entire sample companies have an average of 7% over the 5-year period. Also, data available shows that the TSR of the sample companies has been volatile over the last four years with TSR staying positive until 2017 at 24% (average) and 17% (median) before nosediving to -10% and -12% in 2018. While 2019 looked positive TSR dipped again in 2020. This can be alluded to the impact of the corona virus on business activities.

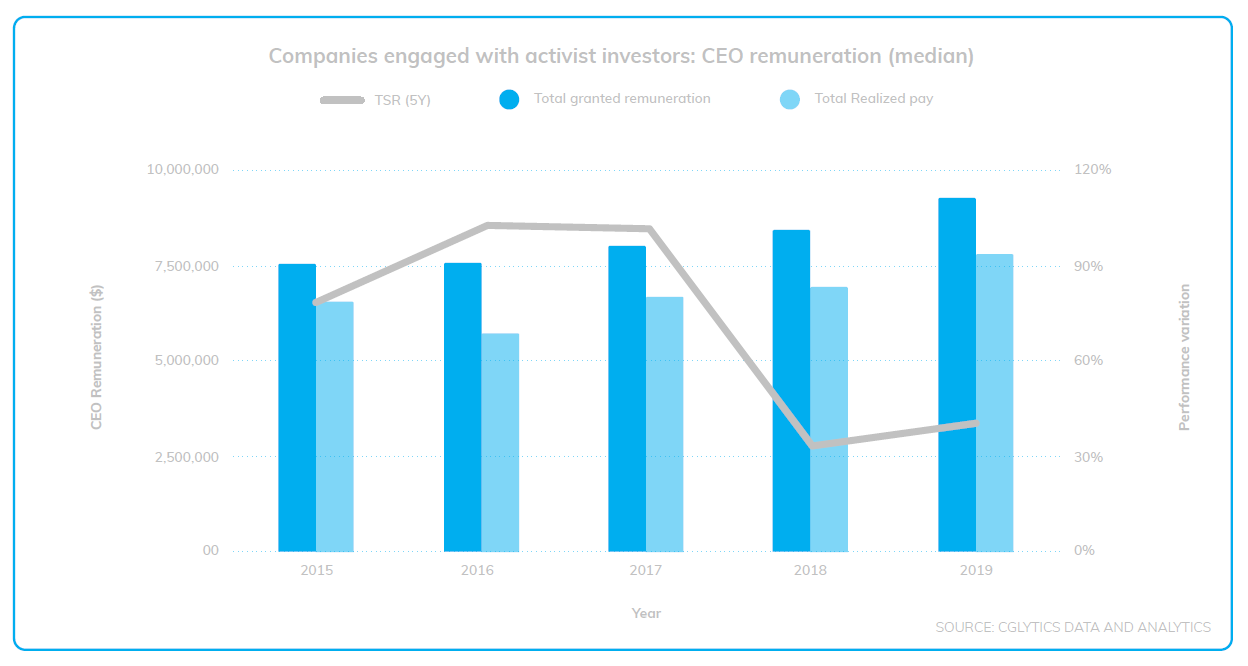

One of the focus areas for activist investors has been executive pay.

Using the CGLytics Pay for Performance modeler, we found that the median total granted compensation for CEOs grew continually from 2015 to 2019, while the year-on-year TSR of the sample companies grew between 2015 and 2017 peaking 101%, then began a downward trajectory from 2017 to 2018 dropping by 68% in 2018, before it picked up in 2019 by 7%. Shareholders increasingly feel that executive pay should be closely linked to performance as well as to ESG issues.

On the other hand, the total realized pay also grew consistently between 2015 and 2019 except for 2016. While TSR dipped between 2017 and 2018 but rose again in 2019 jumping 7%. Over a three-year period, executive compensation consistently outstripped TSR. This reveals that while companies have consistently granted their CEOs generous compensation packages, they are not effectively aligned with their returns to shareholders.

It is apt to say that the hunger for value creation and accretion has not died down. We have seen that the numbers of campaigns so far in half year 2020 is 89% of all campaigns recorded in 2019 and, as mentioned earlier, this is largely driven by factors such as corporate governance, M&A and strategy.

We have seen that majority of the boards within the sample companies have members that will age within the next five years thus will be calling for board refreshment to diversify their age brackets. In terms of expertise brought to the boards we also saw that majority of the boards lack sufficient numbers of directors with technology and governance expertise. These factors attract activist investors or investor activism with the aim to bring about change.

While corporate governance has been the main driver for investor activism over the last four years, it will be wrong to say it is exclusively driven by corporate governance. A single campaign can be driven by multiple factors, as seen in the case of Bed Bath and Beyond, and more recently Elliot Management’s engagement with eBay. This led to board and management changes and review of its strategy thus to the sale of its ticketing division to StubHub.

In a more recent move, Elliot urged NN Group NV to cut cost and overhaul its assets. This includes improving efficiency and shifting some of its investment portfolio from government bonds into corporate bonds. Together, Elliott said, these measures could boost cash flow by €435m a year [5] among other measures.

It is expected that investor activism will continue to be on the rise for the foreseeable future and, as seen in recent years, it is no longer an exclusive club for hedge funds. As such, more variants of investors will be actively involved in investor activism.

The complete publication is available here.